If you think a reduction to the top marginal income tax rate would benefit the top 1% of income earners the most, you would be in the majority of public opinion, but you would also be wrong.

At first thought, it stands to reason that if you give a tax cut to the richest cohort of Australian taxpayers, those in the top marginal income tax bracket, they would be the ones that benefit most, because they are the ones paying a lower rate of tax, but when we analyse the data this is actually not the case.

When the top marginal tax rates are reduced the top 1% of income earners end up paying both more income tax, and a higher proportion of overall income taxes.

But how can that possibly be the case?

We’ll explain in detail below, lets begin:

- A short history of income taxation

- Analysis of income taxes and their impacts

- Incentives drive behaviour, these are the results

- What does this mean for tax policy going forward?

A Short History of Income Taxation

As much as income taxes may seem like a given in today’s modern societies, they are quite a new addition. There are fleeting examples of income taxes being tried at many points in history such as during the Xin Dynasty in 10AD but all were very short lived. The Xin Dynasty’s income tax lasted 13 years until this government was overthrown by the Han Dynasty who immediately repealed the income tax.

The beginning of modern income taxation however is generally accepted as 1799 when the UK introduced their income tax system, which is still in existence today.

That being said, Australia didn’t implement a federal income tax until 1915, just after the USA introduced their federal income tax in 1913, both as a temporary way to raise funds for their respective World War I efforts. Both of which never got removed after the war ended.

Given this, we only have at most 224 years of income tax history and data in the UK, 110 years for the USA and 108 years for Australia.

Analysis of income taxes and their impacts

Although there are copious amounts of data readily available from the ATO, no one yet has done the research on how changes in tax rates in Australia have impacted total taxes collected and the proportions paid by various groups of taxpayers.

On top of this, Australian tax rates have not fluctuated enough to give a good dataset to measure the impacts of varying tax rates. Only having slowly decreased in a largely continuous straight line from 75% in 1942 to 47.5% in 2023.

There is however extensive research done in the USA. And on top of this, their federal income tax rates have fluctuated wildly during their existence from a low of 7% (1913) up to 77% (1918) down to 25% (1928) then up again to 94% (1944) and back down to 28% (1989) up to 43.4% (2017) and down to the 40.8% (2023) it is currently. This gives us an ideal dataset to analyse.

But what this data shows is that every time the top marginal tax rate was increased, the top 1% of income earners paid less tax in gross dollar terms and also in proportion relative to the bottom 99% of taxpayers. And in addition to this, total government income tax revenues declined.

But how, that doesn’t make any sense?

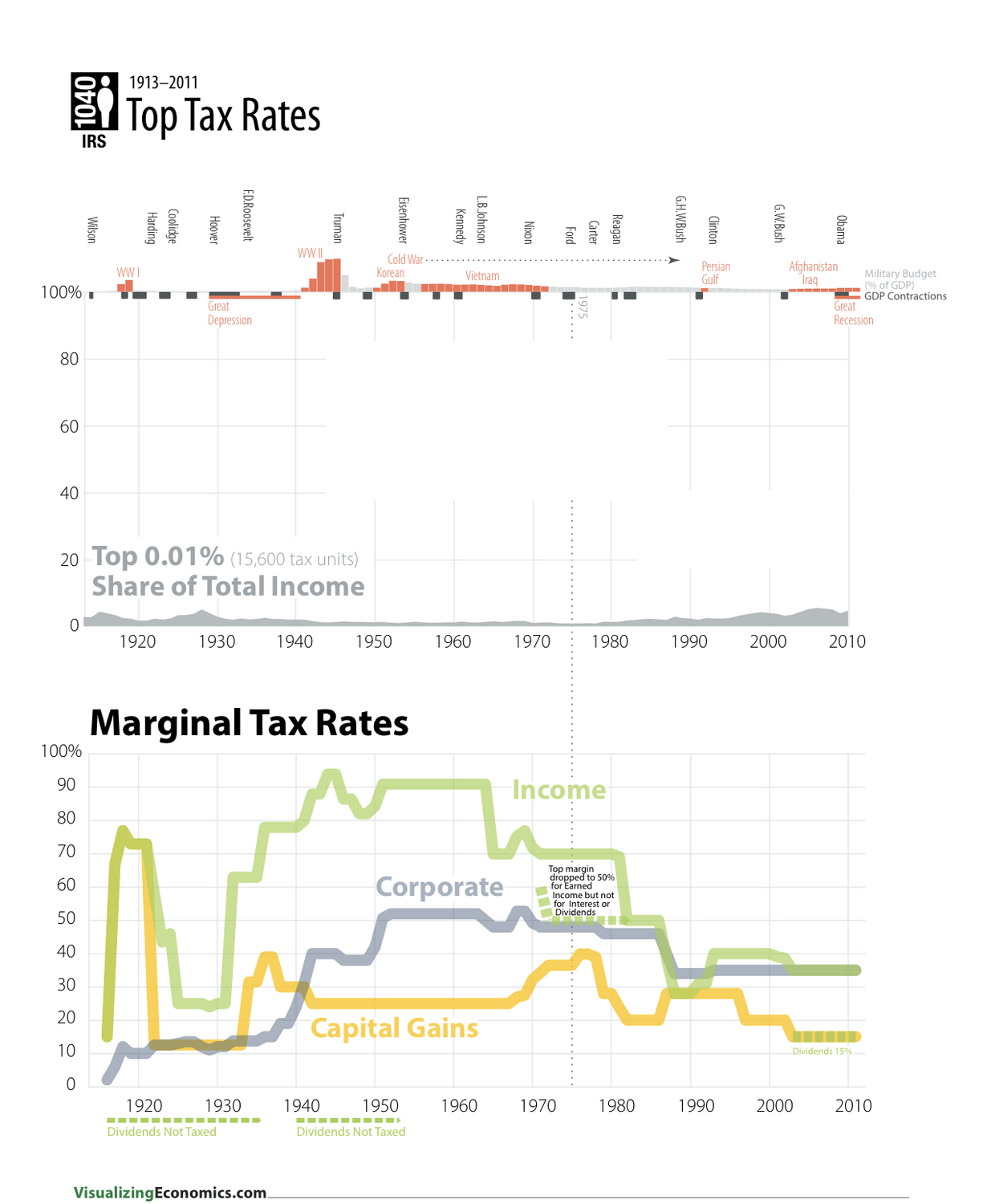

As you can see in the data above, comparing the grey area chart (middle) and the 3 line graphs (Bottom) when tax rates go up the proportion goes down, and when tax rates go down the proportion increases.

- Note this chart shows the proportion of total income taxes paid by the top 0.01%. - The below figures are for the top 1% (taken from USA IRS & Census data included in the book Taxes Have Consequences: An Income Tax History of the United States - Laffer, Domitrovic & Sinquefield):

- In 1917 as soon as the top tax rate was increased from 15% to 67% the percentage of overall taxes paid by the top 1% dropped significantly.

- The low point in this contribution was 38.3% of overall income taxes in 1920 at the peak top tax rate of 73%

- In 1922 the top tax rate started its downward slide from 73% to 24% and the proportion of income taxes paid by the top 1% increased to a peak of 66.66% in 1929 the year of the lowest top tax rate

- From here the top tax rate increased to a maximum of 94% in 1944 and the proportion of income taxes paid by the top 1% dropped like a stone to a low of 13.80% in 1943

- In the 3 years from 1929 to 1931 the amount of tax paid by the top 1% in the USA dropped from $9.8 billion to $2.9 Billion dollars and total income tax revenue dropped from $14.7 Billion to $4.1 Billion

- This correlation between the top tax rate and proportion of total income taxes paid by the top 1% continues all the way through to this day.

Incentives drive behaviour, these are the results of the incentives created by high top tax rates

- The top 1% of income earners are not only the most sensitive taxpayers to tax rate changes as they have the most to lose if unaddressed and they also have the means to make adjustments to their situations

- Incomes earned by the top 1% are the most variable, because those earning this much money don’t desperately need it. Unlike a middle income earner who may need every cent of their paycheck to afford their car or mortgage or private school fees for their children.

- The top 1% can leave money in company structures and only take dividends for the amounts they want to spend, not the total amount they've earned, as they again don’t need all the money

- When the top marginal tax rate is 94% like it was in the USA in 1944 there is a massive incentive to earn less taxable income and to instead switch to earning more tax exempt or more lightly taxed income

- There is also a massive incentive to find great accountants and lawyers who can maximise every loophole and concession available

- In addition there is a massive incentive to find great lobbyists to convince parliament/congress to introduce specific tax concessions that benefit them (for example: green tech credits and electric vehicle rebates)

- The income they do earn will be sheltered away from the people trying to tax it (legally), via onshore company and trust structures, and offshore company and trust structures in tax havens, or by buying assets directly in other family members names instead of their own

- They will also invest in tax exempt government bonds and other tax exempt assets

- Earn income streams taxed at lower rates (capital gains, etc)

- Spend money of their businesses in less efficient ways, just to get a tax deduction, because they bear less of the cost of it being incurred

- Transacting more frequently by barter instead of with fiat money.

The higher the top marginal rate of tax, the larger the incentive to structure your affairs in such a way that you don’t have to pay them.

When the top tax rate is reduced there is less incentive there is to spend as much time rearranging your affairs to minimise tax, and it becomes easier to just pay the taxes and move on, and instead spend more time focusing on earning more money.

For example, let’s compare a taxpayer earning $1M per year, at its peak the USA's top tax rate was 94% this meant that if they earned $1M, they would pay $940,000 in tax and would be left with $60,000 to spend. Now let say they want to engage an accountant to help them minimise their taxes and this costs them $30,000, the decrease in their take home pay is only $1,800 and the decrease in their tax bill is $28,200, effectively the tax office is paying 94% of their accountants fees for them, and if they come up with a solution that saves them just 5% in tax they’ll be left with $106,700 to spend, an almost doubling of the cash they keep

Comparing this to the low point in the USA's top tax rate of 7% they still earn $1M but this time they pay $70,000 in tax and are left with $930,000 to spend. If the accountant can reduce their tax by the same 5% and charges them the same amount of $30,000 the net cost to them is now $29,400 (93% + 5%) of $30,000) and they are left with $950,600, only a marginal increase in the cash they keep

What does this mean for tax policy going forward?

If we are at all serious about raising more revenue for the government to sustain its programs in providing public goods and services, as well as wanting to have a more progressive system where the top 1% of income earners carry a larger portion of the overall income tax burden, then we should support tax policies that lower the top tax rate (such as the stage 3 tax cuts)

But if we are content with shooting ourselves in the feet just so we can flip the bird at the top 1% of taxpayers and get the feeling we are smiting them, knowing full well it is only an illusion and it just serves to benefit them at the expense of low and middle income earners, then we can continue to lobby for the stage 3 tax cuts to be repealed.